Most employers are still waiting for feedback on their TERS applications and accordingly information received to date is fairly limited. The limited feedback to date is that in some instances the TERS benefits received have been far less than what was expected. The purpose of this communication is to provide information based on the benefit calculations that we have seen so far. Our intention is to provide timeous communication on an emerging issue and we do not express opinion as to the legal validity of the calculations received from UIF. We will update this guidance as further information is received, hopefully supported by further legal commentary in due course.

We have noted the following calculation issues in responses received from UIF so far:

- The UIF calculation is based on a number of lock-down days (e.g. 35) whereas most payrolls are being run for the month of April (30 days). The UIF calculation converts all monthly amounts to daily amounts (inclusive of weekend days and public holidays) and will then calculate benefit according to the number of lockdown days as per the application.

- The TERS benefits received for employees who have received partial remuneration is less than expected by some employers. It would appear that the UIF calculation caps the benefit according to the maximum UIF benefit, seemingly negating the impression that employees can receive a further amount from the employer.

- The UIF sliding scale of benefits is difficult to determine in practice.

For employees who have received no remuneration during the lock-down period we do not anticipate major issues, other than possibly some alignment issues between the payroll monthly calculation and UIF calculation based on lockdown days.

For employees who have received some remuneration from the employer, it does seem that there are some complications in practice.

The extracts of the regulations dealing with the TERS benefit to be paid are as follows:

- “Should an employer as a result of the Covid-19 pandemic close its operations, or a part of its operations, for a 3 (three) months or lesser period affected employees shall qualify for a Covid-19 benefit.” (Regulation 3.1)

- “The salary to be taken into account in calculating the benefits will be capped at a maximum amount of R17,712.00 per month, per employee and an employee will be paid in terms of the income replacement rate sliding scale (38%-60%) as provided in the UI Act.” (Regulation 3.4)

- “Should an employee’s income determine in terms of the income replacement sliding scale fall below R3500, the employee will be paid a replacement income equal to that amount.” (Regulation 3.5)

- “Qualifying employees will receive a benefit calculated in terms of Sections 12 and 13 (1) and (2) of the UI Act, provided that an employee shall receive a benefit of no less than R3,500.” (Regulation 3.6)

- “Subject to the amount of the benefit contemplated in clause 3.6, an employee may only receive covid-19 benefits in terms of the Directive if the total of the benefit together with any additional payment by the employer in any period is not more than the remuneration that the employee would ordinarily have received for working during that period.” (Regulation 5.3)

The impression in the above wording is that employees may also earn a portion of remuneration as a supplement to the TERS benefit. An article by Bowmans states that:

“Employers may supplement these benefits, but employees may not get their full salary PLUS the benefit. The maximum that an employee may accordingly receive (from the UIF and their employer) is 100% of her/ his salary.” (https://www.bowmanslaw.com/insights/employment/covid-19-south-african-ters-benefit-what-you-need-to-know/)

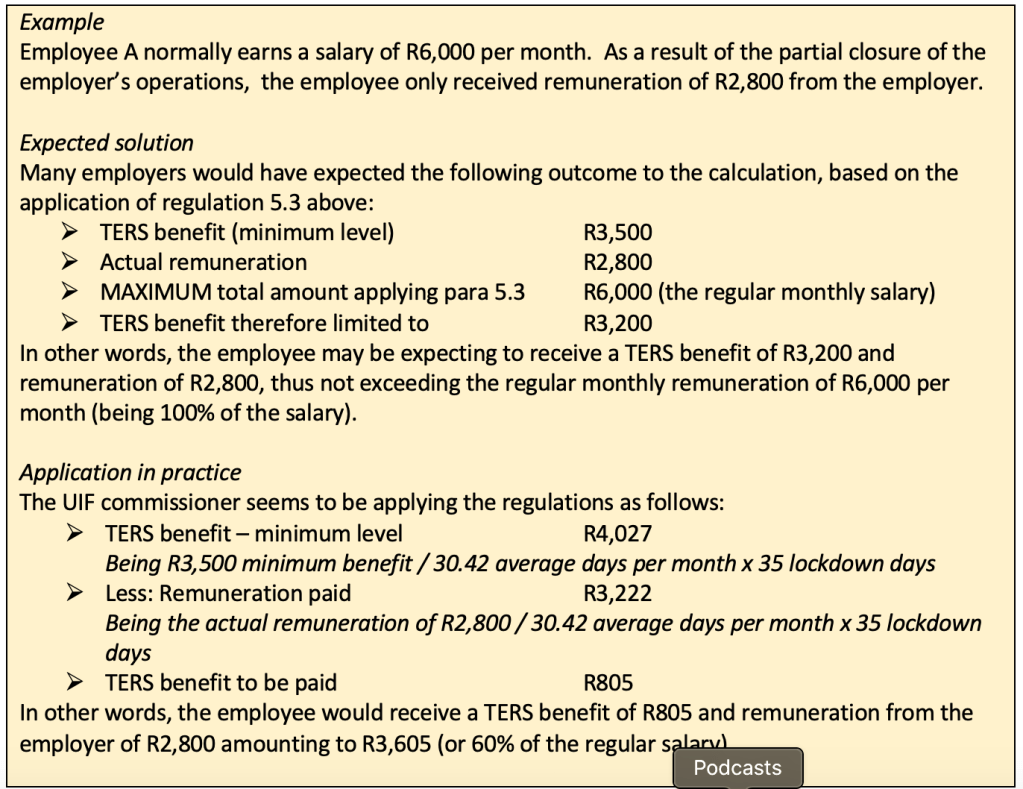

The following example illustrates the formula that is being applied by UIF:

The key point of departure is that many employers would have expected the total received by the employee to be capped at the regular monthly salary (R6,000 in the above example), whereas the UIF calculation caps the total amount at the UIF benefit level (R4,027 in the above example). It is also evident that the application of lockdown days against a monthly salary could cause further smaller anomalies.

The application of the UIF sliding scale is very difficult in practice. Fortunately there are some calculators emerging which get to within a few rand of the determination by UIF and this should be less of an issue going forward.

We have set out further illustrative examples at the footer of this communication, based on actual returned UIF TERS calculations. These examples demonstrate just how technical the UIF process is and will hopefully be of some assistance in interpreting the further responses that will received from UIF.

In practice, for employees whose salary exceeds the calculated UIF benefit, the UIF feedback document will simply state “The Daily Salary Amount is equal to or exceeds the UIF Daily Benefit Amount” (this would apply to employees C and D in the example below). It is clear that the TERS benefit calculations applied by UIF could well result in unexpected hardship for employees, especially if they had understood that the supplementary remuneration received from the employer would be over and above the TERS benefit.

We will monitor situation, particularly further responses received from UIF. A key question will be the legal interpretation of the Regulations and we hope that further insights will be forthcoming in the days ahead. We will communicate again as further insights become available.

You must be logged in to post a comment.