By Peter Cottrell CA(SA)

For many small to medium sized businesses, the primary Covid-19 tax relief will be in the form of a deferral of Employees’ Tax and Provisional Tax liabilities. In many ways this relief represents an interest free source of cash flow from SARS to assist in meeting liquidity requirements. However, there is a potential sting in the tail in that this is a deferral of tax that will require payment in due course. This article will unpack the deferral relief measures in more detail, with illustrations of the practical cash flow implications.

Qualifying Taxpayers

Taxpayers will need to meet the following criteria to qualify for the Employees’ Tax and Provisional Tax deferred payment relief measures (referred to as “Qualifying Taxpayers”):

- Turnover of less than R100 million per annum (initially R50 million);

- Gross income for the year of assessment must not include more than 20%, in aggregate, of interest, dividends, foreign dividends, royalties, rental from letting fixed property, annuities and any remuneration received from an employer; and

- The taxpayer is tax compliant at the time of making the reduced payments.

The turnover amount needs to be determined with reference to a year of assessment ending on or after 1 April 2020 but before 1 April 2021. As this is a forward looking requirement, the turnover criterion is deemed to have been met if the taxpayer’s estimate was seriously calculated and was not deliberately or negligently understated.

We recommend that taxpayers taking advantage of the relief measures keep a record of their projection of turnover, including the factors that were taken into account in formulating the projection. This is particularly important for taxpayers whose turnover is near the R100 million limit.

Deferral of Employees’ Tax

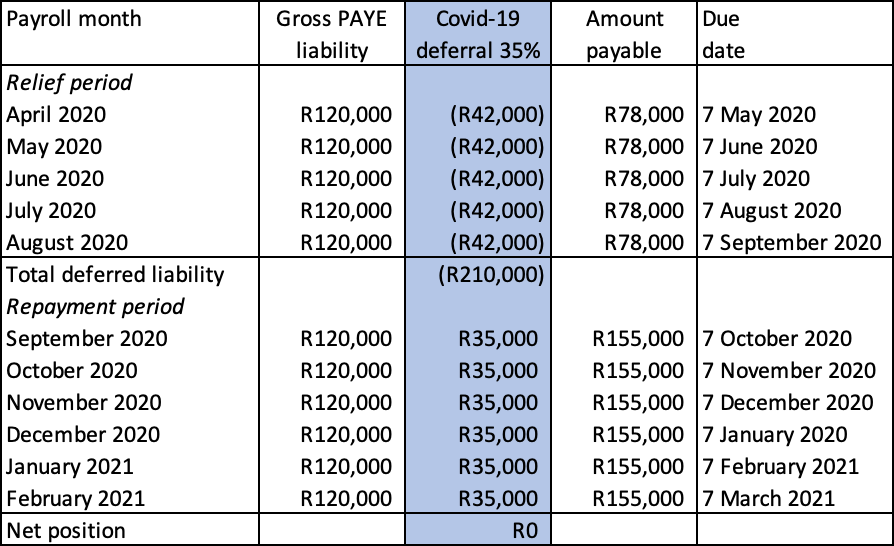

For a six-month period (previously four months), Qualifying Taxpayers are entitled to defer 35% of their employees’ tax (PAYE) liabilities without incurring interest and penalties from SARS. The deferred PAYE liability must be paid to SARS in equal instalments over the six-month period commencing on 1 September 2020 (previously 1 August 2020), with the first payment being made by no later than 7 October 2020.

In practice, the deferral system is working well, and SARS have made changes to the eFiling system such that a “Covid-19 Tax Relief” line appears against each tax period.

The following example illustrates the cash flow implications of the Employees’ Tax Relief:2

Employer A is a small business that meets the qualifying criteria for deferral of employees’ tax. Its gross PAYE liability is R120,000 per month and the effect of the 35% deferral is as follows:

In order to avoid interest and penalties, employers will need to ensure that they have sufficient cash flow available over the months of September 2020 to February 2021 to meet their current employees’ tax obligations together with the repayment of the previously deferred amount.

Deferral of Provisional Tax

For a period of twelve months from 1 April 2020 to 31 March 2021, Qualifying Taxpayers will be entitled to defer a portion of their first and second provisional tax liabilities without incurring interest and penalties. The reduced payments will be determined as follows:

- For first provisional tax payments due between 1 April 2020 and 30 September 2020, payment of 15% of the estimated tax liability for the year (as against the usual 50% of the estimated tax liability);

- For second provisional tax payments due between 1 April 2020 and 31 March 2021, payment of 65% of the estimated tax liability for the year after deduction of the first provisional tax payment (as against the usual 100% of the estimated tax liability).

The payments due per above would be reduced further by any employees’ tax or foreign taxes paid.

The rules with regard to provisional tax estimates of taxable income remain unchanged and are summarised as follows:

For first provisional tax estimates, taxpayers are entitled to use the “basic amount” as the basis for the estimate of income. The basic amount is determined with reference to the last assessed taxable income and an inflation factor will be applied where the tax period is more than eighteen months after the last year of assessment. Use of this estimate will offer a safe haven without risk of penalties, but SARS have discretion to call for current information (for example, management accounts) and may adjust the estimate if they determine that a higher estimate is required. Conversely, the estimate amount may be reduced should circumstances justify a lower amount, but SARS has the right to call for supporting documentation and may impose penalties if the Commissioner is not satisfied with the support for the lower estimate.

For second provisional tax estimates, the basis for determination of the estimate is dependent on the level of taxable income:

- Taxpayers with a taxable income of less than R1 million may make use of the basic amount as a safe haven. A reduced estimate may be made, but a penalty will be incurred if that estimate is less than 90% of the final taxable income.

- Taxpayers with a taxable income of more than R1 million will be required to make an accurate estimate of income for the year. A penalty will be incurred if the estimate is less than 80% of the final taxable income.

The balance of the tax due for the year of assessment will be payable as a top-up payment. For taxpayers with February year ends, the top-up payment is due by no later than 30 September 2021. For other year ends, the top-up is due within six months of the tax year end.

Taxpayers who have been adversely affected by the impact of Covid-19 will need to give careful consideration to the estimates of taxable income as used for provisional tax purposes. Where reduced estimates are applied, taxpayers will need to ensure that the estimate has been carefully considered and that supporting documentation is available.

The following examples illustrate the application of the provisional tax rules and the deferred payment arrangements:

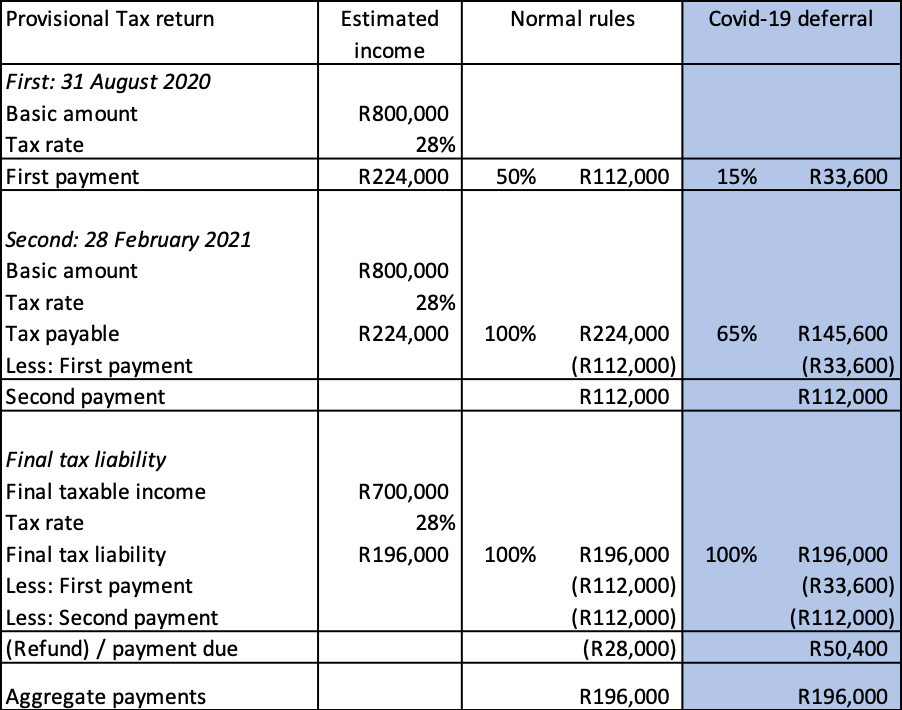

Example 1 – Basic illustration of relief measure

Taxpayer A is a qualifying company and has a February year end. The last assessed income is R800,000 (basic amount) and the final taxable income for the year ended 29 February 2021 is R700,000. Assuming that the company uses the basic amount estimates, provisional tax will be payable as follows:

The above illustrates that the taxpayer would receive cash flow relief in August 2020 even if a reduced estimate is not applied. A top-up payment would need to be made by 30 September 2021 in order to avoid interest being levied by SARS on the outstanding balance due.

While welcoming the additional liquidity offered by the relief measures, taxpayers will need to bear in mind that the top-up payments will fall due around the same time that the first provisional tax payments for the following tax year are due.

Example 2 – “catch-up” effect

We now look at the position for the months August 2021 and September 2021, with facts as for example 1, and assuming that the basic amount remains at R800,000. The tax cash flows will be as follows:

- 31 August 2021 – First provisional tax payment for the February 2022 = R800,000 x 28% x 50% = R112,000

- 30 September 2020 – Third provisional tax payment for the February 2021 tax year payable by 30 September 2021 = R50,400 (as calculated above per example 1)

- Total payments = R162,400 (as against R112,000 that would have applied without the deferral relief measures)

In practice, the “catch-up” effect of the previously deferred provisional tax payments could place considerable pressure on cash flow in the subsequent financial year.

Further illustrative examples are included at the footer of this article illustrating application of different scenarios.

Of course, all of the above pre-supposes that the taxpayer will have taxable income at the end of the tax year. Some industries and sectors have been so badly affected that they will have a tax loss. In these instances the provisional tax estimates will be reduced to zero and the relief measures are of no consequence as there will be no tax payable. Unfortunately this is the nature of a tax relief measure, but this does not provide comfort to some of the businesses that are facing greatest adversity.

Conclusion

The Employees’ Tax and Provisional Tax deferred payment relief measures could provide considerable liquidity benefit to taxpayers in the short-term. However, careful cash flow planning will be required to ensure that the taxpayer has sufficient funds available to meet future tax obligations.

References

1 Treasury Media Statement 31 July 2020 – Publication of the 2020 Draft Tax Bills

2 Modified from an example as published in the Disaster Management Tax Relief Administration Bill B12-2020.

FURTHER ILLUSTRATIVE EXAMPLES

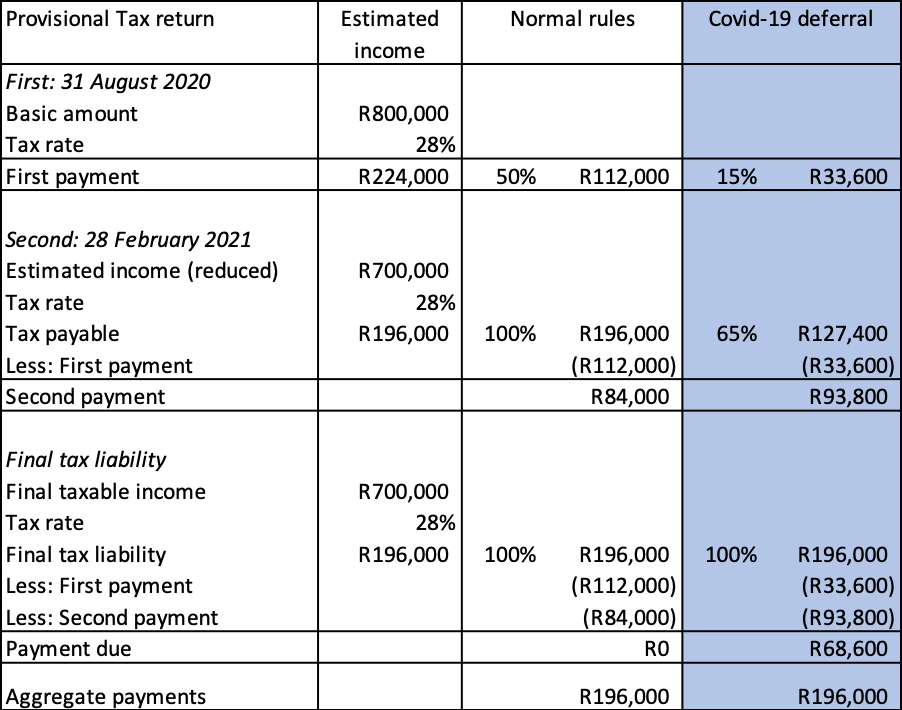

Example 3 – Reduced estimate

Taxpayer A is a qualifying company and has a February year end. The last assessed income is R800,000 (basic amount) and the final taxable income for the year ended 29 February 2021 is R700,000. Assuming that the company uses the basic amount for the first payment and makes a reduced estimate for the second payment, provisional tax will be payable as follows:

In applying a reduced estimate the company achieves further cash flow relief in February 2021, but will need to make a higher top-up payment in September 2021. However, the company will have had to make an accurate estimate of income in order to reduce the risk of penalties.

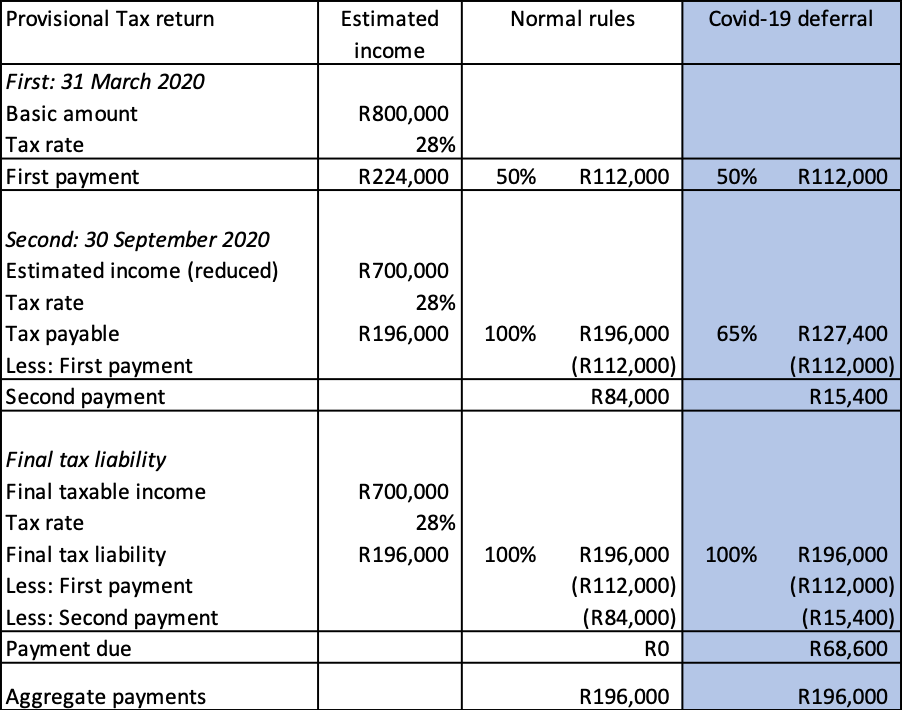

Example 4 – A different year endTaxpayer B is a qualifying company and has a September year end. The last assessed income is R800,000 (basic amount) and the final taxable income for the year ended 30 September 2020 is R700,000. The company used the basic amount for its first payment that was due on 31 March 2020 and the Covid-19 relief measures did not apply, meaning that 50% of the estimated liability was paid. Assuming the company makes a reduced estimate for the second payment, provisional tax will be payable as follows:

As the relief measures did not apply to the first provisional tax payment, the company will enjoy cash flow relief for the purposes of its second payment in September 2020. A top-up payment will be required in March 2021 in order to avoid interest.

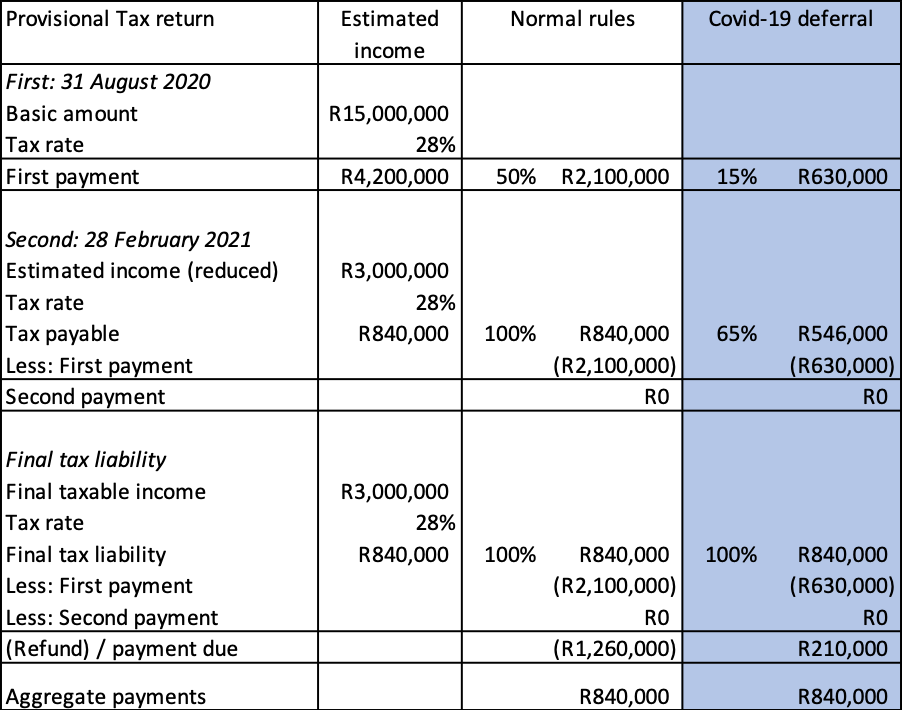

Example 5 – Significantly reduced income

Taxpayer C is a qualifying company and has a February year end. The last assessed income is R15 million (basic amount), but the company’s operations have been badly impacted by Covid-19 and the final taxable income for the year ended 28 February 2021 is only R3 million. Assume that the company elects to use the basic amount for the first payment. An accurate estimate will be required for the second payment as the estimated taxable income is greater than R1 million. Provisional tax will be payable as follows:

The above example illustrates that aside from the cash flow benefit, the Covid-19 relief rules also take much uncertainty out of the first provisional tax process. Use of the basic amount offers a safe haven for the purposes of the provisional tax return and in many cases this will still apply notwithstanding the decline in income. For taxpayers who face a reduction in taxable income of more than 85%, then a reduced estimate may well need to be made. However, the income estimate will need to be carefully considered and documented in order to avoid the risk of penalties.

You must be logged in to post a comment.