By Peter Cottrell CA(SA)

Since our update on 24 April, much progress has been made with the TERS benefit UIF calculations and by now most employers will have received a second round of payments from UIF. The purpose of this communication is to provide an update on the current status benefit calculations and implementation issues.

Benefit Calculations

For employees who did not receive any remuneration in the month of April, the benefit calculation has been relatively straightforward. However, for employees who did receive remuneration, the first round of benefit payments from the UIF were far less than expected. The expectation was that the sum of the TERS benefit and remuneration received would be capped at the regular monthly remuneration that the employee would have received. The first round of payments capped the amount at the maximum UIF benefit.

The UIF fund recognised that there were issues with the calculation and automatically recalculated the benefits due to employees, resulting in a second round of top-up payments. This is very good news both for employers and employees. The updated calculations applied by UIF are available for download from the UIF Covid-19 web site, although we are aware that some clients have not yet received those calculation

In reviewing the calculations for the second round of payments we have found that, in some instances, the total TERS benefits received have now exceeded the expected amount. Paragraph 5.3 of the Regulations reads as follows:

“Subject to the amount of the benefit contemplated in clause 3.6, an employee may only receive covid-19 benefits in terms of the Directive if the total of the benefit together with any additional payment by the employer in any period is not more than the remuneration that the employee would ordinarily have received for working during that period.”

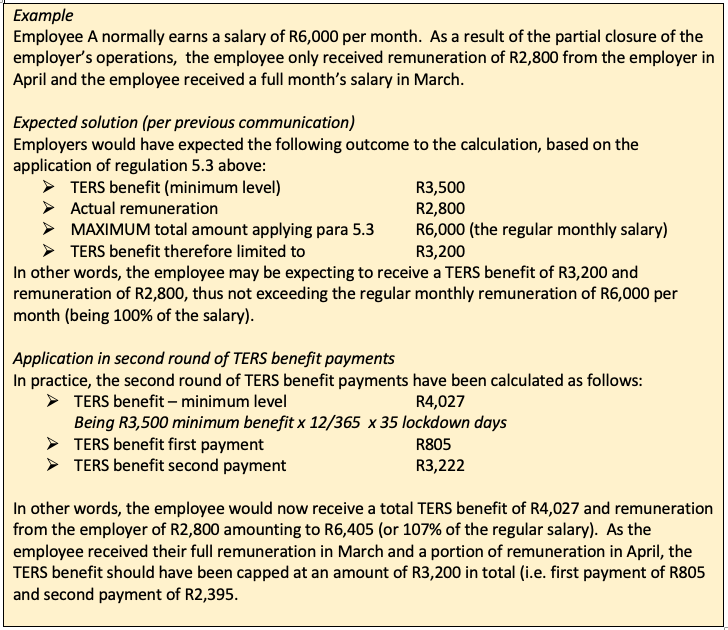

From the calculations we have received so far, it would appear that the capping to the remuneration that the employee would ordinarily have received has not taken place. This is illustrated by updating the example used in our previous communication:

In our interpretation of the regulations, the sum of the TERS benefit and the remuneration paid by the employer should not have exceeded the regular monthly salary paid by the employer. In practice, the impact of this is on employees who have received part remuneration from the employer in salary bands of up to about R20,000 per month.

This raises a practical issue as to how to deal with the surplus. In practice, most employers will have already paid the TERS benefit to employees prior to receipt of even the first round payments. This approach was urged by paragraph 5.5 of the Regulations:

“To speed payment of COVID 19 benefits to employees, employers are urged to pay employees based on clause 3.4 of the Directive and to reimburse or set off such with COVID 19 benefits claim payments from UIF.”

We are working with clients on a case by case basis as to how to deal with these excess amounts. We draw attention that in terms of the regulations employers may not hold these amounts for their own benefit.

Implementation Issues

Now that payment of TERS benefits has been made, employers will need to ensure that their accounting, record keeping and data submissions are up to date in terms of the Memorandum of Agreement (MOA) that was signed with UIF. We draw attention to the following requirements:

- The notification letter received from UIF contains an acceptance to be signed by the employer. It should be noted that this acceptance includes an authority for UIF to obtain direct confirmation or verification from the employer’s bank that the employees have been paid the salaries and benefits as indicated in the application.

- The employer must pay employees their benefits within two days of receiving funds from the UIF (Clause 11 of MOA).

- The employer must submit proof of payment to the UIF within five days of receipt of funds from UIF (Clause 12 of MOA). In practice, the information to be submitted to UIF will include:

- The breakdown report received from TERS showing the list of employees and amount received (if this has been received, we are aware that some have not received this as yet).

- Where there has been an overpayment, we would recommend that a reconciliation is prepared between the TERS breakdown report showing the capped amount (to be paid to employee), amount paid by TERS and the overpayment.

- For employers who have included TERS in their payroll run, the payslip(s) showing the TERS benefit and salary split.

- Proof of payment/bank statement agreeing to net salary paid (payslip).

- If not yet included in the payroll, proof of payment/bank statement agreeing the payment made to employee to the TERS breakdown report or reconciliation.

- The employer must return any unutilised funds, including interest, to the UIF within ten days of the recommencement of its business operations, or the termination of the revised MOA, whichever is the earlier.

It is essential that employers are diligent in their record keeping in order to avoid the risk of breach of the MOA and having to pay funds back to UIF.

Peter Cottrell CA(SA)

STRATEGIC BUSINESS SUPPORT

Email: peter@bizsupport.co.za | Telephone: +27 31 7613400 |

Web: www.bizsupport.co.za

You must be logged in to post a comment.